Traditional IRAs

A traditional individual retirement account (IRA) is a personal savings plan that offers certain tax benefits to encourage retirement savings.

What is it?

The basics

A traditional individual retirement account (IRA) is a personal savings plan that offers certain tax benefits to encourage retirement savings. Contributions to traditional IRAs are either tax deductible (the money goes into the IRA pre-tax) or nondeductible (you

pay income tax on the money that goes into the IRA). Regardless of whether your contributions are tax deductible, amounts contributed to a traditional IRA grow tax deferred inside the IRA.

A traditional IRA is not itself an investment, but a tax-advantaged vehicle in which you can hold some of your investments. You need to decide how to invest your IRA dollars based on your own tolerance for risk and investment philosophy. How fast your IRA dollars grow is largely a function of the investments you choose to fund the IRA.

Tip: The term "IRA" can refer either to an individual retirement account or an individual retirement annuity. An individual retirement annuity is an annuity or endowment contract that you purchase from a life insurance company. The contract must not be transferable, and the premiums must be flexible so that if your compensation changes, your premium payments can also change. In general, the same rules that apply to individual retirement accounts also apply to individual retirement annuities.

Caution: This discussion pertains only to traditional IRAs. Roth IRAs are subject to different rules

Caution: Special rules apply if you inherit an IRA.

Caution: Special rules apply to certain distributions to reservists and national guardsmen called to active duty after September 11, 2001.

Deductible contributions

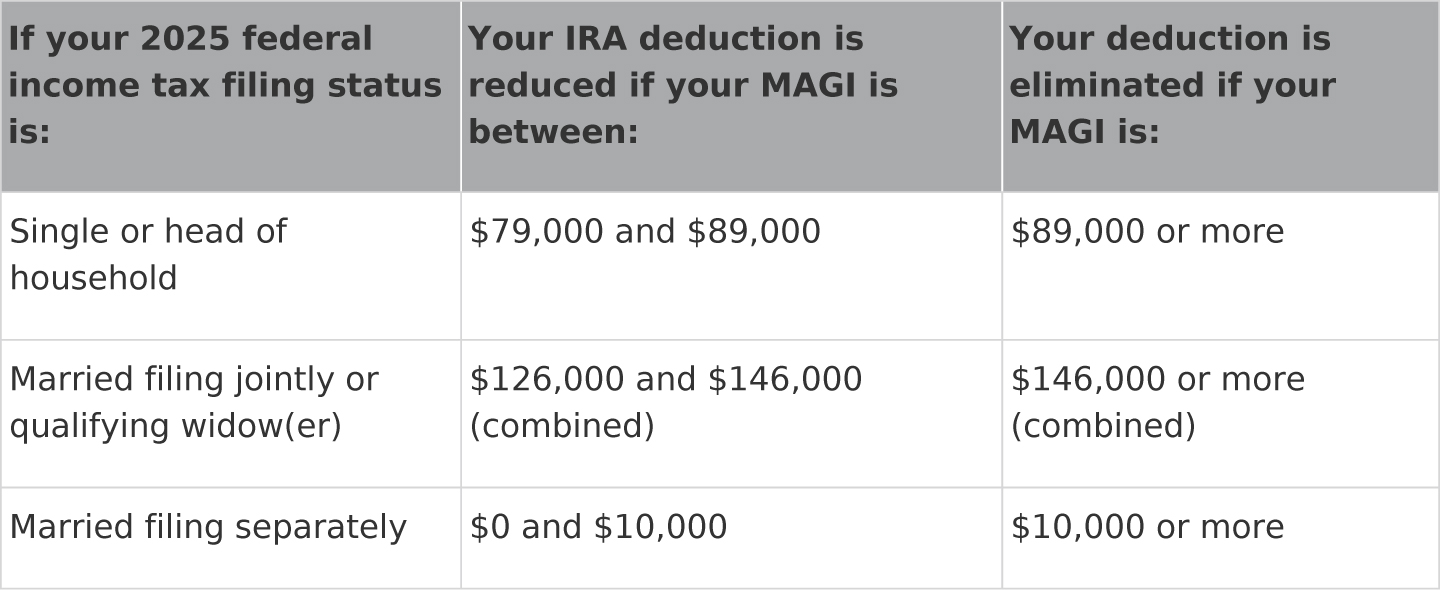

When you make tax-deductible contributions to a traditional IRA, the money you invest in the IRA is pre-tax. Tax-deductible contributions are pre-tax because they reduce your taxable income on your federal income tax return. You can contribute up to the lesser of $7,000 or 100% of your taxable compensation to a traditional IRA in 2025 (unchanged from 2024). If neither you nor your spouse is covered by an employer sponsored retirement plan, your entire contribution can be tax deductible. If one of you is covered by such a plan, the amount of deductible contribution you can make (if any) depends on your modified adjusted gross income (MAGI) and federal income tax filing status for the year (see table below).

Tip: Making deductible contributions to a traditional IRA often makes sense if you expect to be in a lower income tax bracket when you retire.

Nondeductible contributions

If you or your spouse is covered by an employer-sponsored retirement plan, you might not be able to deduct all (or any) of your traditional IRA contribution. But you can still contribute up to the annual contribution limit (or your taxable compensation for the year, if less), even if part or all of your contribution is not deductible (and therefore not pre-tax). Contributions that you make to a traditional IRA that you cannot deduct on your federal income tax return are referred to as nondeductible contributions (see table below).

Tip: If you are eligible to contribute to a Roth IRA there is generally no advantage to making nondeductible contributions to a traditional IRA.

When can it be used?

You must receive taxable compensation during the year

To contribute to an IRA (traditional or Roth), you must receive taxable compensation during the year. For purposes of IRA contributions, taxable compensation includes wages, salaries, commissions, self-employment income, and taxable alimony or separate maintenance. Other taxable income, such as interest earnings, does not qualify as taxable compensation for this purpose. Your contribution for a given year cannot exceed your taxable compensation for that year.

Tip: Members of the Armed Forces may include nontaxable combat pay as part of their taxable compensation when determining how much they can contribute to an IRA (their own or a spousal IRA). For service members with only nontaxable combat pay, Roth IRA contributions will generally make more sense than nondeductible contributions to a traditional IRA.

Tip: Differential pay received by service members is considered compensation for IRA contribution purposes. Differential pay is defined as any payment which: (1) is made by an employer to an individual with respect to any period during which the individual is performing service in the uniformed services while on active duty for a period of more than 30 days; and (2) represents all or a portion of the wages that the individual would have received from the employer if the individual were performing services for the employer.

Tip: You don't need taxable compensation in order to make rollover contributions to your traditional IRA, or repayments of qualified reservist distributions.

If you (and your spouse) are not covered by an employer-sponsored retirement plan, contributions are fully deductible

If neither you nor your spouse is covered by an employer-sponsored retirement plan [e.g., a pension, profit-sharing plan, 401(k) plan], you can generally deduct the full amount of your traditional IRA contribution on your federal income tax return. If you are covered by such a plan, your ability to make deductible IRA contributions depends on your MAGI and federal income tax filing status for the year (see table below). You are considered covered by an employer-sponsored retirement plan if you were covered by such a plan for even one day during the year. You are also considered covered by such a plan if you were eligible to participate in the plan but chose not to do so.

If you are covered by an employer-sponsored retirement plan, your ability to deduct your contribution depends on your modified adjusted gross income and your filing status

If you are covered by an employer-sponsored retirement plan and your MAGI exceeds certain established thresholds, your deduction for your traditional IRA contribution is reduced or eliminated as follows:

These income ranges (other than married filing separately) are indexed for inflation each year.

If you are married, special rules may apply

If you are covered by an employer-sponsored retirement plan, it doesn't matter whether your spouse is covered by such a plan — your ability to deduct your IRA contributions is subject to the income limits described above. If, however, you are not covered by an employer-sponsored retirement plan but your spouse is covered by such a plan, special rules must be followed to determine the deductible portion (if any) of your traditional IRA contribution:

- If you file your federal income tax return as married filing jointly and your combined MAGI in 2025 is $236,000 or less, you can make a fully deductible contribution to a traditional IRA.

- If you file as married filing jointly and your combined MAGI in 2025 is between $236,000 and $246,000, you can make a partially deductible IRA contribution. See Questions & Answers.

- If you file as married filing jointly and your combined MAGI in 2025 is $246,000 or more, you cannot deduct any portion of your traditional IRA contribution. See Questions & Answers.

- If you file your federal income tax return as married filing separately but lived with your spouse at any time during the year, your ability to make deductible IRA contributions is limited. If you file as married filing separately but did not live with your spouse at any time during the year, you are considered a single taxpayer for purposes of determining the deductible portion (if any) of your IRA contribution.

Tip: If you are married filing a joint return, you may be able to contribute to an IRA for your spouse, even if he or she has little or no taxable compensation.

Strengths

Contributions can be made on a pre-tax basis

Assuming you qualify for deductible contributions to a traditional IRA, those contributions are made on a pre-tax basis. In other words, the deductible portion of your IRA contribution reduces your taxable income on your federal income tax return. You don't have to pay federal income tax on your deductible contribution amounts until you withdraw those amounts from the traditional IRA.

IRA funds grow tax deferred

Funds in a traditional IRA, including investment earnings, are not taxed until they are distributed to you. This tax deferral greatly increases the growth potential of your IRA. With earnings compounding tax deferred year after year in the IRA, you will generally end up with a larger balance than if you invested the same amount in a taxable investment at the same rate of return.

IRA investment choices are broad and diverse

You can establish an IRA with a bank, mutual fund company, life insurance company, or stock brokerage firm. You can even have multiple IRA accounts with more than one institution (though your total contribution to all of your IRAs cannot exceed the annual limit). Furthermore, you can choose from a wide range of specific investments to fund your IRA. Intense competition for IRA dollars has led to a large number of IRA providers and investment choices.

Caution: All investing involves risk, including the possible loss of principal. Before investing in any mutual fund, carefully consider its investment objectives, risks, fees, and expenses, which are discussed in the prospectus available from the fund. Read the prospectus carefully before investing.

State and federal laws may provide protection from creditors

Many states shield IRAs from creditors. You should check with an attorney to find out how your state treats IRAs. However, while the protection given to funds in an IRA is generally greater than that given to non-IRA investments, it is usually significantly less than that given to funds held in qualified retirement plans. Federal law provides protection for up to $1,711,975 (scheduled for adjustment in April 2028) of your aggregate Roth and traditional IRA assets if you declare bankruptcy. [SEP IRAs, SIMPLE IRAs, and amounts rolled over to the IRA from an employer qualified plan or 403(b) plan, plus any earnings on the rollover, aren't subject to this dollar cap and are fully protected if you declare bankruptcy.] The laws of your particular state may provide

additional bankruptcy protection, and may also provide protection from the claims of your creditors in cases outside of bankruptcy. (Inherited IRAs may be afforded less protection from creditors under federal and state law — seek professional guidance.)

May increase income-sensitive deductions

Assuming you qualify for deductible IRA contributions, that portion of your contribution reduces your taxable income on your federal income tax return. When you reduce your taxable income in this manner, other deductions that are income sensitive (such as medical expenses that exceed 7.5% of your adjusted gross income) may increase, providing additional tax benefits.

A traditional IRA is relatively simple to maintain

Unlike qualified employer-sponsored retirement plans, there are no annual reporting requirements for IRAs or for deductible contributions made to IRAs. (There are some record keeping and paperwork requirements associated with nondeductible contributions made to a traditional IRA.)

Contributions are discretionary

You do not have to make a contribution to your IRA for any given year unless you choose to. Within the limits on the amount that you can contribute each year, you can exercise complete discretion in deciding how much and when to save.

“Catch-up” contributions are allowed if you’re at least 50

Individuals age 50 and older may make an additional yearly catch-up contribution of up to $1,000 in 2025 (unchanged from 2024) to a traditional or Roth IRA (over and above the regular contribution limit). The purpose of this provision is to help older individuals increase their savings as they approach retirement.

You may qualify for a tax credit

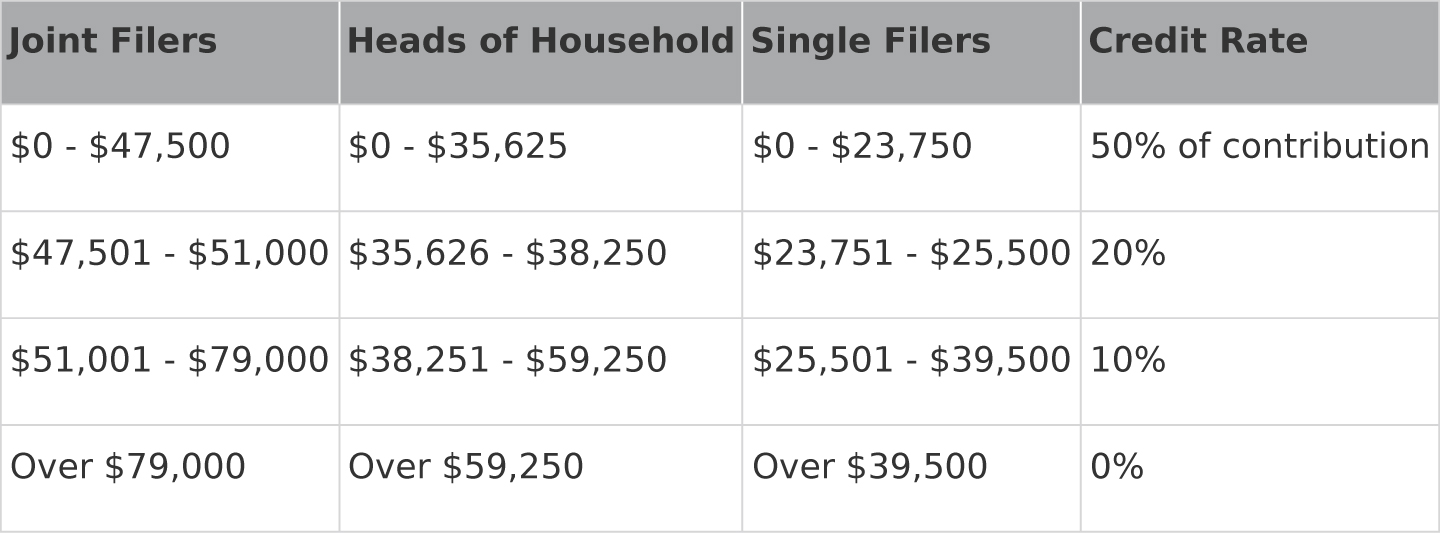

Certain low- and middle-income taxpayers can claim a partial, nonrefundable income tax credit for amounts contributed to a traditional or Roth IRA. The maximum amount of the credit is 50%, 20%, or 10% of your contributions up to $2,000 ($4,000 if married filing jointly). The actual amount of the credit (if any) depends on your MAGI. Here are the credit rates, based on 2024 MAGI limits (these limits are indexed annually for inflation):

To claim the credit, you must be at least 18 years old and not a full-time student or a dependent on another taxpayer's return. The credit is in addition to any income tax deduction you might qualify for with respect to your IRA contribution.

Caution: The amount of any contribution eligible for the credit may be reduced by any taxable distributions you (or your spouse if you file a joint return) receive from an IRA or employer-sponsored retirement plan (or any nontaxable distributions from a Roth IRA) during the same tax year, during the period for filing your tax return for that year (including extensions), or during the prior two years.

Note: In 2026, the Saver's Credit will be replaced by a Saver's Match. Instead of a credit applied to a taxpayer's income tax obligation, a matching contribution equal to 50% of the taxpayer's investment amount (up to a $2,000 maximum per individual) will be deposited into the taxpayer's IRA or retirement plan. Phaseout limits will apply.

Tradeoffs

Your ability to make deductible contributions to an IRA may be reduced or eliminated if you are covered by an employer-sponsored retirement plan

As discussed above (see table), if you are covered by an employer-sponsored retirement plan, your ability to make deductible contributions to a traditional IRA depends on your MAGI and tax filing status for the year.

If your spouse is covered by an employer-sponsored retirement plan but you are not, special rules apply

You are not considered covered by an employer-sponsored retirement plan merely because your spouse is. However, if your spouse is covered by such a plan (and you are not) and your combined MAGI exceeds a certain amount (see "If you are married, special rules apply" above), your ability to make deductible contributions to a traditional IRA is either limited or eliminated. If your spouse is covered by an employer sponsored retirement plan and you file separate returns, your ability to make a deductible contribution is severely limited.

Funds you withdraw from a traditional IRA may be taxable income in the year received

When you make deductible contributions to a traditional IRA, the money that you are investing in the IRA is pre-tax. Once in an IRA, the funds grow tax deferred. However, when you take funds out of the IRA, those deductible contribution amounts will be subject to federal income tax in the year distributed to you. Similarly, any investment earnings will be subject to federal income tax in the year distributed. Only nondeductible contribution amounts will not be taxed when distributed, since those dollars were taxed once already.

Taxable income is taxed at ordinary income tax rates even if funds represent long-term capital gains or qualifying dividends

Long-term capital gains are generally subject to tax at rates that are lower than ordinary income tax rates. Additionally, qualifying dividends paid to individual shareholders from domestic corporations (and qualified foreign corporations) are taxable at the lower long-term capital gains tax rates as well. Distributions from tax deferred accounts that represent such long-term capital gains and dividends, however, will not enjoy this tax benefit — they are taxable at ordinary income tax rates.

Distributions made before you reach age 59½ may be subject to a 10% penalty tax

An IRA is a retirement savings vehicle, and the tax law encourages you to use the money in the IRA for that purpose. Although a number of exceptions exist, a 10% premature distribution tax generally applies to the taxable portion of any distribution that you take from a traditional IRA before reaching age 59½. This penalty tax is in addition to regular federal income tax.

Your beneficiaries pay income tax on proceeds received after your death

Someone has to pay the income tax on the assets in your IRA, and if it's not you, it's probably going to be your beneficiaries (unless your beneficiary is a charity). After you die, in addition to any estate tax that might be due, the funds in your traditional IRA will eventually be subject to federal income tax at your beneficiary's rate (to the extent that those funds include deductible contributions and investment earnings). However, because taxable IRA death benefits payable to your beneficiary constitute "income in respect of a decedent," or IRD, your beneficiary may be entitled to an income tax deduction equal to the estate taxes that are attributable to the IRA.

Contributions are limited to the annual maximum

Your total contribution to all of your IRAs (traditional and Roth) cannot exceed $7,000 in 2025. If you're age 50 or older by the end of the calendar year, you can contribute an extra $1,000 in 2025 due to a "catch-up" contribution provision. However, this is still considerably less than the contribution limits for most employer-sponsored retirement plans.

Tip: You may also be able to contribute up to the annual limit in your spouse's name, plus a catch-up contribution if he/she is age 50 or older, even if your spouse has little or no taxable compensation.

Caution: An active reservist or guardsman who receives a qualified reservist distribution can repay all or part of that distribution to an IRA at any time during the two-year period beginning on the day after active duty ends. The regular IRA contribution limits don't apply to these repayments (and the repayments aren't deductible).

Tip: The annual contribution limits don't apply to rollover contributions.

You must begin to take annual minimum withdrawals from your IRA when you reach age 73 (or 75)

You are required to take annual minimum withdrawals (required minimum distributions) from a traditional IRA after you reach age 73 (75 for those who reach age 73 after December 31, 2032). You can always withdraw more than the required minimum in any year. These withdrawals are calculated based on your life expectancy, and are intended to dispose of all of the money in the IRA over a given period of time. In contrast, Roth IRAs are not subject to required minimum distribution rules during your lifetime.

How to do it

Establish an IRA

Where you choose to establish your IRA and the specific investments you choose depend on your own personal needs and preferences. You have a wide variety of choices, and you should carefully consider the matter before making your decision. How fast your IRA dollars grow is more a function of investment strategy and performance than of tax deferral. Consider whether you want to establish an IRA with a:

- Bank

- Financial institution

- Mutual fund company

- Brokerage firm

- Life insurance company

You should also consider the types of investments (e.g., stocks, bonds, mutual funds, CDs, annuities) that will best suit your goals and risk tolerance. Finally, keep in mind that you can establish multiple IRA accounts with more than one institution.

Caution: All investing involves risk, including the possible loss of principal. Before investing in a mutual fund, carefully consider the investment objectives, risks, charges, and expenses of the fund. This information can be found in the prospectus, which can be obtained from the fund. Read it carefully before investing.

Tip: Employers who maintain certain retirement plans [like 401(k), 403(b), or 457(b) plans] can allow employees to make their regular IRA contribution — traditional or Roth — to a special account set up under their retirement plan. These accounts, called "deemed IRAs," function just like regular IRAs. Advantages include the fact that your retirement assets can be consolidated in one place, contributions can be made automatically through payroll deduction, you can take advantage of any special investment opportunities offered in your employer's plan, and your protection from creditors may be greater than that available in a standalone IRA. The downside is that the investment choices in your employer's plan may be very limited in comparison to the universe of investment options available to you in a separate IRA. Also, the distribution options available to you and your beneficiaries in a deemed IRA may be more limited than in a standalone IRA. Because of the administrative complexity involved, most employers have been reluctant to offer these arrangements. Check with your plan administrator to see if this is an option for you.

You have until the due date of your federal tax return for the year (usually April 15) to make a contribution for that year

If you want to make an IRA contribution for the year, you have until the due date of that year's federal income tax return. For most people, this is usually April 15 of the following year. The period of time you have to make a contribution is not extended by any extension you may receive to file your return. So, if you obtain an automatic four- month extension, you may have additional time to file your return, but you don't have any additional time to make an IRA contribution.

Tip: You can direct the IRS to deposit all or part of your federal income tax refund directly to an IRA (subject to the normal rules governing the amount, timing, and deductibility of IRA contributions).

Designate the year for which the contribution is made

If you contribute to your IRA after December 31, you should tell the IRA trustee or custodian for which year the contribution is being made. For instance, if you make a contribution in March 2025 for the 2024 tax year, you should clearly identify the contribution as being made for 2024. Otherwise, the trustee or custodian may assume that the contribution is for the year in which it is received and report it as such. Talk to your IRA trustee or custodian about how you should identify your contribution.

Deduct your contributions on your individual federal income tax return

If you qualify to make deductible contributions to a traditional IRA, make sure that you calculate the portion of your annual contribution that is deductible. Then make sure that you deduct that amount on your federal income tax return. You take a deduction on your federal income tax return for the year for which you make the IRA contribution.

Tip: You can claim a deduction for IRA contributions before you actually make them. For instance, assume you qualify to make a deductible contribution to a traditional IRA for 2025. You can file your 2025 return in March 2026 and claim an IRA deduction even though you may have not yet actually contributed the money. You can wait until April 15 of 2026 to contribute to your IRA so you can actually use your federal income tax refund to fund the contribution (assuming you receive your refund in time).

Verify contributions you make to your IRA

Your IRA trustee or custodian should send you a Form 5498 (or a similar statement). This form or statement, usually sent by June, will show you all of the contributions made to your IRA for the previous year. Check it carefully, particularly if you made a contribution after the close of the calendar year. If there seems to be a problem, contact your advisor or your IRA trustee or custodian immediately.

Investment choices appropriate for IRAs

Remember that an IRA is not itself an investment, but a tax-advantaged vehicle in which you can hold some of your investments. Choosing specific investments to fund your IRAs is an important decision. Here are some points to keep in mind:

- You need to decide how to invest your IRA dollars based on your own retirement goals, tolerance for risk, investment philosophy, time horizon, and other personal factors

- How fast your IRA dollars grow is largely a function of the investments that you choose, as well as tax deferral

- There are specific types of investments that you cannot use to fund your IRAs (such as life insurance), and there are some choices that usually make more sense as IRA investments than others (e.g., mutual funds, CDs)

- If you're unhappy with your IRA investment choices, you can typically move your money to other investments offered by the same financial institution, or to a different institution

- You should consider any fees associated with opening and maintaining your IRA

Caution: The IRS has ruled that the wash sales rules apply if you sell stock or other securities outside of your IRA for a loss, and purchase substantially identical stock or securities in your IRA (traditional or Roth) within 30 days before or after the sale. The result is that you cannot take a deduction for your loss on the sale of the stock or securities. In addition, your basis in your IRA is not increased by the amount of the disallowed loss.

Tax considerations

Income Tax

Deductible contributions reduce your taxable income

Any deductible IRA contributions you make reduce your taxable income on your federal income tax return for the year if the contribution is made or on or before the tax-filing deadline for that year (usually April 15 of the following year).

Nondeductible contributions are made with after-tax dollars

Unlike deductible contributions, nondeductible contributions to a traditional IRA are made with after-tax dollars and do not reduce your taxable income for the year. However, your nondeductible contribution amounts will not be subject to federal income tax when you eventually withdraw them from the IRA.

IRA investments grow tax deferred

Funds in an IRA grow tax deferred. You do not pay any federal income tax on those funds as long as they remain inside the IRA.

Distributions from a traditional IRA may be included in your taxable income

Distributions from a traditional IRA are subject to federal income tax to the extent that those distributions consist of deductible contributions and investment earnings (the portion of a distribution that represents nondeductible contributions is not taxed, as those dollars were already taxed). Such distributions are taxable at ordinary income tax rates even if they represent long-term capital gains or dividends that would otherwise qualify for capital gains tax treatment. This is true both as you take distributions during your life, and when distributions are made to your beneficiaries after your death.

A 10% penalty tax can be assessed on withdrawals you make prior to age 59½

Distributions you take prior to reaching age 59½ are potentially subject to a 10% premature distribution tax. This penalty tax is in addition to any regular federal income tax that might apply. There are a number of exceptions to the penalty, however.

Rollovers

In general, a rollover is the movement of funds from one retirement savings vehicle to another — in this case, from one traditional IRA to another. Rollovers are treated separately from contributions; you are still allowed to make your regular IRA contribution in a year when you have a rollover transaction. There are no age restrictions regarding rollovers, but there are other specific rules that must be followed. If properly completed, rollovers are not subject to income tax or the premature distribution tax. There are two possible ways that IRA funds can be rolled over, a 60- day (or indirect) rollover and a trustee-to-trustee transfer (or direct rollover).

Tip: You can roll over funds from a traditional IRA to another traditional IRA or you can roll over funds from a Roth IRA to another Roth IRA. Special rules apply to converting or rolling over funds from a traditional IRA to a Roth IRA. See "Converting or rolling over traditional IRAs to Roth IRAs," below. You may also be able to roll over taxable funds from an IRA to an employer-sponsored retirement plan, and vice-versa.

With a 60-day rollover, you actually receive a distribution from your traditional IRA. To complete the rollover transaction, you make a deposit into the IRA that you want to receive the funds. You must deposit the full amount distributed to you within the allowable 60-day period. If you fail to complete the rollover or miss the 60-day deadline, all or part of your distribution will be subject to income tax and possibly the premature distribution tax.

Caution: You can make only one tax-free, 60-day, rollover from one IRA to another IRA in any one-year period no matter how many IRAs (traditional, Roth, SEP, and SIMPLE) you own. This does not apply to direct rollovers (trustee-to-trustee transfers), or Roth IRA conversions.

When you take a distribution from your traditional IRA, your IRA trustee or custodian will generally withhold 10% for federal income tax (and possibly additional amounts for state tax and penalties) unless you instruct them not to. If tax is withheld and you then wish to roll over the distribution, you have to make up the amount withheld out of your own pocket. Otherwise, the rollover is not considered complete, and the shortfall is treated as a taxable distribution. The best way to avoid this outcome is to instruct your IRA trustee or custodian not to withhold any tax. Unlike distributions from qualified plans, IRA distributions are not subject to a mandatory withholding requirement.

The second type of rollover transaction occurs directly between the trustee or custodian of your old traditional IRA, and the trustee or custodian of your new traditional IRA. You never actually receive the funds or have control of them, so a trustee-to-trustee transfer is not treated as a distribution (and therefore, the issue of tax withholding does not apply). Trustee-to-trustee transfers avoid the danger of missing the 60-day deadline, and are not subject to the "once-per-12-month" limitation.

You may qualify for a tax credit

If you're a low- or middle-income taxpayer, you may qualify for a partial income tax credit for amounts contributed to a traditional or Roth IRA. See the Strengths section for details.

Qualified health savings account (HSA) funding distribution

If you are covered by a high deductible health plan (HDHP), you may be able to make a nontaxable HSA funding distribution from your traditional IRA that would otherwise be included in income. The distribution must be a direct trustee-to-trustee transfer to an HSA. The distribution will be nontaxable to the extent it is not more than the limit on your annual HSA contributions. Generally, you can make only one nontaxable HSA funding distribution during your lifetime. However, if you change your HDHP coverage from self-only to family, you may be able to make an additional distribution during the same year. For more information, see IRS Publication 553.

Gift and Estate Tax

When you die, your IRA is included in determining if estate tax is due

Unless you name your spouse as beneficiary (unlimited marital deduction) or a charity as beneficiary (charitable deduction), the full value of your IRA at the time of your death is added to your other assets to determine if federal gift and estate tax is due. In addition, your state may impose a state death tax.

Questions & Answers

What is a traditional IRA?

A traditional IRA is a personal savings plan that offers certain tax advantages to encourage you to set aside money for your retirement. Depending on your circumstances, you may be able to deduct all or part of your traditional IRA contributions, thereby reducing your taxable income on your federal income tax return. Funds in a traditional IRA grow tax deferred, meaning that you pay no taxes as long as the funds remain inside the IRA.

Caution: Roth IRAs, under which contributions aren't deductible but qualified distributions are tax free, are discussed elsewhere. This discussion pertains specifically to traditional IRAs.

Who can set up a traditional IRA?

You can set up a traditional IRA and make contributions if you received taxable compensation during the year. For purposes of this discussion, taxable compensation includes wages and salaries, commissions, self-employment income, and taxable alimony or separate maintenance. Taxable compensation does not include earnings and profits from property (such as rental income, interest income, and dividend income), pension or annuity income, deferred compensation received, or any items that are excluded from income.

Tip: You can also establish a traditional IRA to accept rollover contributions from an employer-sponsored retirement plan or from another traditional IRA, regardless of your age or the amount of your taxable income.

What is a spousal IRA?

If you meet certain conditions, you can set up and contribute to an IRA for your spouse, even if he or she received little or no taxable compensation in the year of the contribution. Such an IRA is referred to as a spousal IRA. To contribute to a spousal IRA for any year, you must meet four conditions:

- You must be married at the end of the year

- You must file a joint federal tax return for the year

- You must have taxable compensation for the year

- Your spouse's taxable compensation for the year (if any) must be less than yours

You can contribute up to the limit for both yourself and your spouse, including catch-up contributions that may apply, provided you have earned income at least equal to the total contribution amount.

How much can you contribute to an IRA?

You can make contributions to your traditional IRA for each year that you qualify, up to annual limits. To qualify to make contributions, you must have received taxable compensation during the year.

Tip: Contribution limits don't apply to rollover contributions or repayment of qualified reservist distributions.

Are your contributions deductible?

Unmarried individuals: If you are not covered by an employer-sponsored retirement plan, you can deduct the full amount of your traditional IRA contribution. If you are covered by an employer-sponsored retirement plan, your ability to deduct your contributions depends on your MAGI for the year.

If you are married, different rules apply. See "When can it be used?" above for details.

Are you covered by an employer-sponsored retirement plan?

An employer-sponsored retirement plan, for purposes of the IRA deduction rules, is any of the following:

- A qualified pension, profit-sharing plan, stock bonus plan, or money purchase pension plan (including Keogh plans)

- A 401(k) plan

- A union plan (a qualified stock bonus, pension, or profit-sharing plan created by a collective bargaining agreement between employee representatives and one or more employers)

- A qualified annuity plan

- A plan established for its employees by the United States, by a state or political subdivision, or by any instrumentality of these entities (not including Section 457 eligible state deferred compensation plans)

- A Section 403(b) plan (a tax-sheltered annuity plan for employees of public schools and certain tax-exempt organizations)

- A simplified employee pension (SEP) plan

- A savings incentive match plan for employees (a SIMPLE plan)

If you are not sure if you are covered by an employer-sponsored retirement plan:

- Check your Form W-2. If you are covered by such a plan, your Form W-2 for the year should have the "Retirement plan" box checked.

- Ask your employer.

You are generally considered to be covered by a defined contribution plan (e.g., profit sharing plan, stock bonus plan, money purchase pension plan) if amounts are contributed or allocated to your account (even if you haven't yet vested in those contributions). You are generally considered to be covered by a defined benefit plan if you're eligible to participate in the plan, even if you choose not to do so, and even if you haven't accrued a benefit. You are not considered covered by an employer sponsored retirement plan simply because your spouse is covered by such a plan. However, if your spouse is covered by such a plan and you are not, special rules apply.

Other special rules:

- Member of a reserve unit of the armed forces: If you are a member of a reserve unit of the armed forces, you are not considered covered by an employer sponsored plan if the plan was established by a government agency (the United States, a state, a political subdivision or instrumentality), and you do not serve on active duty (not counting training) for more than 90 days during the year.

- Volunteer firefighter: If the only reason that you are covered by an employer sponsored retirement plan is because you are a volunteer firefighter, you will not be considered covered if the plan was established by a government agency, and your accrued retirement benefits will not provide more than $1,800 per year upon retirement.

If you are covered by an employer-sponsored retirement plan, how do you calculate the amount of your deductible IRA contribution (if any)?

You must first calculate your MAGI. Your MAGI is the amount of AGI shown on page 1 of your Form 1040 or 1040A, without taking into account any:

- IRA deduction

- Foreign-earned income exclusion

- Foreign housing exclusion or deduction

- Exclusion of Series EE bond (may also be called Patriot bond) interest shown on Form 8815

- Exclusions of employer-provided adoption assistance

- Student loan interest deduction

Next, check your MAGI against the income phase-out ranges based on your filing status. See the chart above in "Are your contributions deductible?"

If your IRA deduction is reduced and not completely eliminated, you must calculate the portion of your IRA contribution that is deductible. A worksheet is available to help you make this calculation. See IRS Publication 590-A, Individual Retirement Arrangements (IRAs).

What if your spouse is covered by an employer-sponsored retirement plan, but you are not?

It depends upon your filing status:

- Married filing jointly: You are not considered covered by an employer-sponsored retirement plan simply because your spouse is covered by such a plan. However, if you are not covered by an employer-sponsored retirement plan, but your spouse is, your traditional IRA deduction is reduced or eliminated if your income exceeds certain limits. See "If you are married, special rules may apply" above.

- Married filing separately: If you file your federal income tax return as married filing separately and your spouse is covered by an employer-sponsored retirement plan, your traditional IRA deduction is reduced if your MAGI is between $0 and $10,000, and eliminated if $10,000 or more.

Tip: If you are married but did not live with your spouse at any time during the year, and you file separate returns, you are considered a single taxpayer for purposes of determining the deductible portion of your traditional IRA contribution.

What is the limit on nondeductible contributions to a traditional IRA?

The difference between the maximum amount you can contribute to a traditional IRA for a given year and the amount of your deductible contributions for that year is the amount that you can make as a nondeductible contribution.

If you want to, you can also designate a deductible contribution to a traditional IRA as a nondeductible contribution by reporting the contribution as nondeductible on your federal income tax return.

Tip: If you are eligible to contribute to a Roth IRA there is generally no advantage to making nondeductible contributions to a traditional IRA.

Caution: Repayments of qualified reservist distributions are not deductible.

Do you have to report nondeductible contributions?

Yes. For any year that you make a nondeductible contribution to a traditional IRA, you must file IRS Form 8606 with your federal income tax return. You must report nondeductible contributions on Form 8606 even if you do not have to file a federal tax return for the year. You must also file Form 8606 for any year that you take a distribution from your traditional IRA if you have ever made nondeductible contributions.

Caution: If you do not report nondeductible contributions, all of your traditional IRA contributions will be treated as deductible. This means that when you make

withdrawals, all of the money you withdraw from the IRA will be taxable unless you can prove to the IRS's satisfaction that nondeductible contributions were made. A penalty can be charged if you do not file Form 8606 when required, or if you overstate the amount of your nondeductible contributions on Form 8606.

If you make nondeductible contributions to a traditional IRA, does this affect distributions you take from the IRA?

Yes. If you make nondeductible contributions to a traditional IRA, you have a cost basis in the IRA. Nondeductible contributions are not subject to federal income tax when they are distributed to you, because you already paid tax on those dollars and they are considered a return of your investment in the IRA. Once you have made a nondeductible contribution, withdrawals from the IRA are considered made partly from your nondeductible contributions and partly from deductible contributions and investment earnings. You should consult your tax advisor with regard to this situation.

How do you calculate the taxable and nontaxable portions of a distribution if you make nondeductible contributions?

If you make nondeductible contributions to a traditional IRA, you calculate and report the taxable and nontaxable portions of a distribution using IRS Form 8606. Basically, Form 8606 calculates the ratio of your nondeductible contributions to your total IRA balance, and applies that ratio to any distribution made. For instance, if 50% of your IRA balance represents nondeductible contributions, half of your distribution would be subject to federal income tax, but the half representing nondeductible contributions would not be. All of your traditional IRAs are aggregated for this purpose.

What acts will result in penalties, and what if you contribute too much to an IRA (excess contributions)?

Prohibited transactions: Improper use of an IRA by you, your beneficiary, your fiduciary, or members of your family will result in loss of beneficial tax status. Improper use includes:

- Borrowing money from the IRA (although you can in effect withdraw money from your IRA and pay it back within 60 days without tax or penalty by taking advantage of IRA rollover rules — once in any 12-month period)

- Selling property to the IRA

- Receiving unreasonable compensation for managing the IRA

- Using the IRA as security for a loan

- Buying property for personal use with IRA funds (you can always withdraw money from your IRA to purchase property for personal use — the problem arises when you try to invest your IRA funds in such property)

Investment in collectibles: If your IRA invests in collectibles, the amount invested is considered distributed to you in the year invested. In addition to federal income tax, you may have to pay the 10% tax on premature distributions. Collectibles include artwork, rugs, antiques, metals, gems, stamps, coins, alcoholic beverages, and certain other tangible personal property.

Caution: There is an exception. Your IRA can invest in one, one-half, one-quarter, or one-tenth ounce U.S. gold coins or one-ounce silver coins minted by the U.S. Treasury Department.

Tip: You can also invest your IRA assets in certain platinum coins and in gold, silver, platinum, or palladium bullion of a minimum fineness. The bullion must, however, be in the physical possession of the IRA trustee or custodian.

Excess contributions: If you contribute more than you are allowed to for any year and do not withdraw this overcontribution (and any earnings attributable to the overcontribution) by the due date of your federal income tax return for that year (including extensions), you are subject to a 6% tax. The 6% tax, calculated on Form 5329, is assessed on the amount of excess contributions remaining in your IRA at the end of the tax year.

Early withdrawals: Unless an exception applies, withdrawals taken prior to age 59½ are subject to a 10% premature distribution tax on the taxable portion of the withdrawal.

Required distributions after age 73: After you reach age 73 (75 for those who reach age 73 after December 31, 2032), you must begin to take annual required minimum distributions from your traditional IRA. A 50% excise tax is assessed on amounts that you are required to distribute but do not.

This content has been reviewed by FINRA.

Prepared by Broadridge Advisor Solutions. © 2025 Broadridge Financial Services, Inc.